PPFAS Mutual Fund has set up a dedicated subsidiary — PPFAS Alternate Asset Managers IFSC Private Limited — inside GIFT City (Gujarat International Finance Tec-City). Through this entity, it now offers dollar-denominated funds that give Indian investors an uncapped route into US equities.

This guide covers what these funds are, who can invest, the exact steps to get started, and the costs and tax rules you need to know before you commit money.

What is GIFT City, and why does it matter?

GIFT City, in Gandhinagar, Gujarat, is India’s first International Financial Services Centre (IFSC). It operates differently from a regular Indian fund jurisdiction in three key ways:

- Regulated by the IFSCA (International Financial Services Centres Authority), not SEBI.

- Units set up there are treated as non-resident entities under India’s foreign exchange rules.

- Funds from GIFT City can invest abroad without the overseas investment ceiling that domestic Indian mutual funds face.

The overseas investment cap has repeatedly frozen fresh subscriptions to international mutual funds in India — once the industry-wide RBI/SEBI limit is hit, fund houses simply pause new investments. GIFT City offers a structurally different, parallel route around that bottleneck entirely.

What PPFAS is offering from GIFT City

PPFAS has launched two passive, outbound Fund-of-Funds (FoFs) through its GIFT City subsidiary:

Accumulating

Accumulating

How both funds work:

- Feeder structure — they don’t buy US stocks directly. They invest 90–100% of pooled money into accumulating ETFs and UCITS funds tracking the respective indices.

- Accumulating share class — dividends are reinvested automatically rather than paid out. No annual dividend income to declare; cleaner tax compliance.

- Small remainder (0–10%) held in debt or money market instruments for liquidity.

PPFAS has also indicated plans for an inbound feeder fund (for NRIs to access the Parag Parikh Flexi Cap Fund) and PMS offerings from the same GIFT City entity. For now, only the two FoFs above are open for investment.

Who can invest?

- Resident Indian individuals — the primary investor category, investing under the RBI’s Liberalised Remittance Scheme (LRS).

- Other entities permitted under IFSCA rules — corporates, trusts, partnership firms, HUFs.

The S&P 500 and Nasdaq 100 FoFs are structured for resident Indians under LRS — not for NRIs. PPFAS’s planned inbound fund (feeding into the Flexi Cap Fund) is the route being built for NRIs. Investing in the wrong structure could create compliance issues.

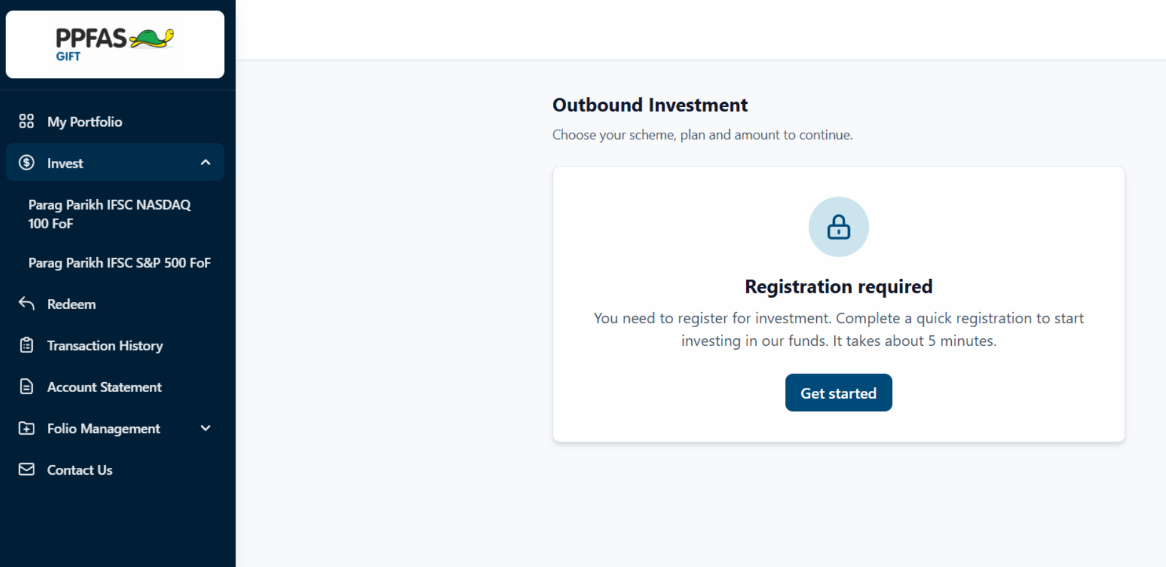

How to Invest in PPFAS GIFT City Funds (Step-by-Step)

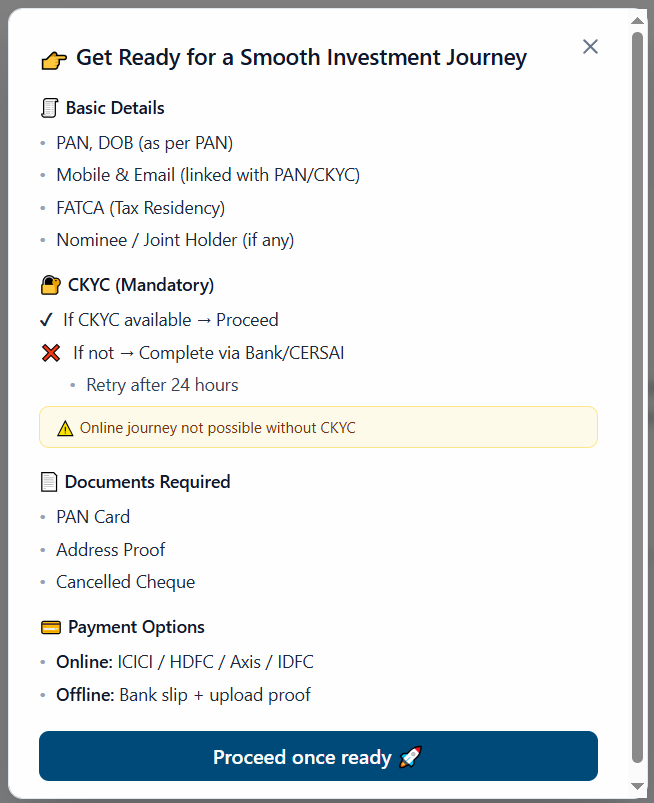

Your existing PPFAS mutual fund folio does not automatically work for the GIFT City platform. Registration, CKYC verification and onboarding are completed separately through the dedicated PPFAS GIFT City portal.

Step 1: Register on the PPFAS GIFT City Portal

Visit gift.ppfas.com/gift-invest/signup and create your account.

- PAN

- Date of Birth (as per PAN)

- Mobile Number

- Email Address

- FATCA / Tax Residency details

- Nominee details (optional)

Step 2: Complete CKYC Verification

The portal validates your CKYC status before allowing investments.

- PAN Card

- Address Proof

- Cancelled Cheque

Proceed immediately with the investment process.

If CKYC is unavailable, complete CKYC through your bank, broker or CKYC registration process and retry after it is updated.

Step 3: Select Your Fund

After onboarding, navigate to the Invest section from the left menu and choose your preferred scheme.

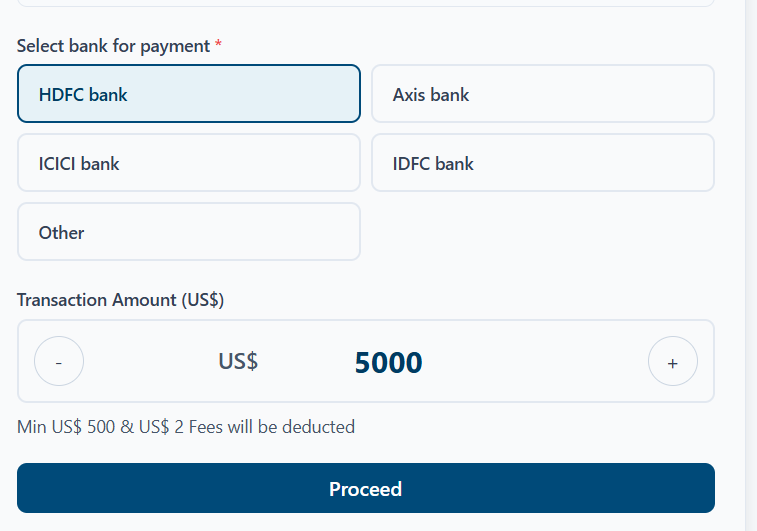

Step 4: Choose Bank and Investment Amount

Select your bank and enter the amount you wish to invest.

| Bank | Process |

|---|---|

| ICICI Bank | Online |

| HDFC Bank | Online |

| Axis Bank | Online |

| IDFC Bank | Online |

If your bank is not listed, choose Other and use the Remit Now / Internet Banking route.

Step 5: Complete Remittance

Your investment is made under the Liberalised Remittance Scheme (LRS). Forex conversion charges, bank charges and TCS rules may apply depending on your annual remittances.

Some investors have reported competitive exchange rates through ICICI Bank on the PPFAS portal. Compare rates before remitting and do your own research.

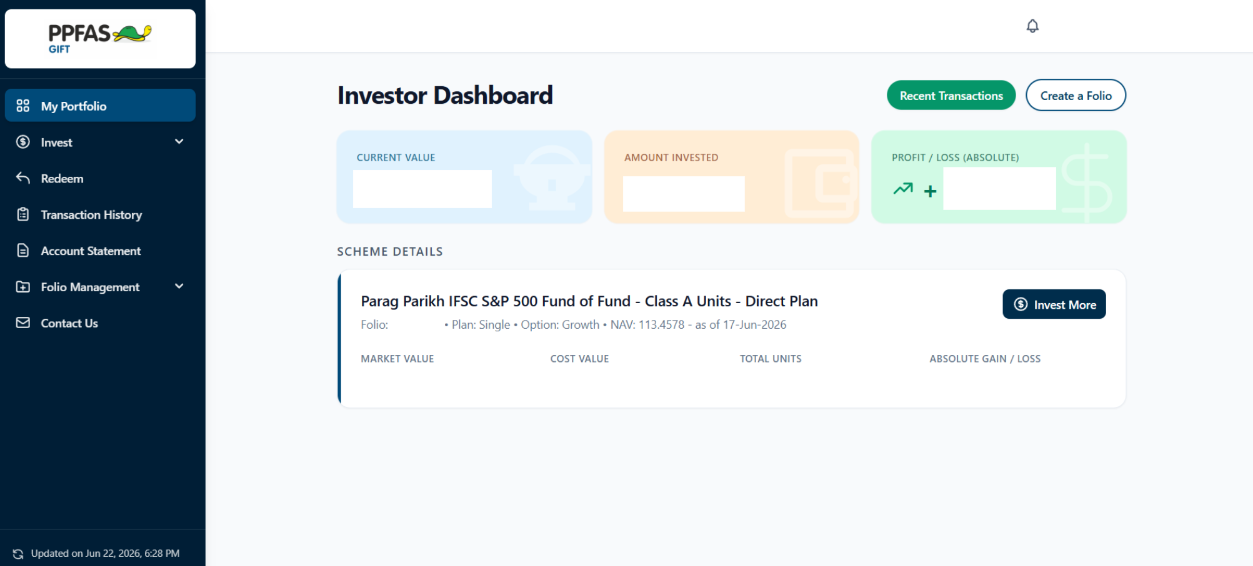

Step 6: Track Your Portfolio

Once units are allotted, your dashboard displays current value, amount invested, gains/losses, units held and transaction history. Additional investments can be made using the Invest More option.

Investments count toward your annual USD 250,000 LRS limit. Maintain records of remittances and consult your tax advisor regarding Schedule FA reporting requirements.

Minimum investment and costs

PPFAS set the $5,000 floor deliberately so that a first investment stays below the ₹10 lakh annual LRS threshold at which 20% TCS kicks in. The overall cost structure:

| Cost item | S&P 500 FoF | Nasdaq 100 FoF |

|---|---|---|

| Scheme expense ratio | ~0.30% | ~0.30% |

| Total expense ratio (incl. underlying ETF) | ~0.40% | ~0.55% |

| Exit load | Nil | Nil |

| Per-transaction fee | US$2 per remittance | US$2 per remittance |

| Lock-in period | None | None |

| NAV publication frequency | Daily (USD) | Daily (USD) |

| Redemption settlement | USD to your bank account | USD to your bank account |

One important limit to track: any remittance also counts against your overall LRS limit of USD 250,000 per financial year, shared across all foreign remittances including travel, education, and other investments.

Tax rules you need to know

GIFT City funds are taxed very differently from a regular Indian mutual fund. There are four distinct things to understand:

1. Fund-level taxation — not investor-level

Capital gains tax is paid inside the fund before the NAV is published. You do not compute or pay capital gains on redemption.

| Holding period | Tax treatment inside fund | Effective rate |

|---|---|---|

| Under 2 years | Taxed at slab rates | Up to ~42.75% (incl. surcharge & cess) |

| Over 2 years | Long-term capital gains | ~14.95% effective |

2. TCS on your LRS remittance

TCS (Tax Collected at Source) is deducted by your bank on LRS remittances exceeding ₹10 lakh in a financial year. It is not an extra tax — it can be claimed back or offset against your income tax liability — but it is a real cash outflow at the time of investment. Plan your remittance amounts and timing accordingly.

3. Schedule FA — the open question

Whether resident investors must disclose GIFT City fund holdings under Schedule FA (Foreign Assets) in their ITR is genuinely debated among tax professionals. GIFT City is treated as an offshore jurisdiction under FEMA, which creates the ambiguity. Given the steep penalty for non-disclosure:

Most advisors recommend filing Schedule FA as a precaution until clearer regulatory guidance is issued. Consult a CA before filing your ITR. See our complete Schedule FA guide →

4. No US estate tax

Because the funds invest through UCITS structures — not directly in US-domiciled stocks or ETFs — they fall entirely outside the scope of US estate tax. Direct investors with over $60,000 in US-situs assets face up to 40% estate tax as Non-Resident Aliens. The UCITS wrapper eliminates this risk. Learn more about the US estate tax trap →

How GIFT City compares to other routes

| Feature | PPFAS GIFT City FoFs | Domestic Indian MFs | Direct US Investing |

|---|---|---|---|

| Capital gains tax | Paid inside fund; NAV is post-tax | You pay on redemption | You pay yourself |

| US estate tax risk | None (UCITS structure) | None (Indian domicile) | Up to 40% above $60,000 |

| Access to fresh money | Always open | Frequently frozen at RBI/SEBI limit | Open |

| Compliance burden | Medium (TCS + Schedule FA) | Low | High (FATCA, foreign filings) |

| Min. ticket | $5,000 | ₹500 SIP | Varies by broker |

Key risks to weigh

- Currency risk — returns are exposed to INR–USD movements in both directions. A weakening rupee boosts your rupee returns; a strengthening rupee erodes them. No hedging mechanism inside the fund.

- Nasdaq 100 concentration — heavily weighted toward large technology companies. More upside in tech-led rallies, sharper drawdowns when the sector corrects. The S&P 500 is broader and comparatively more diversified.

- Regulatory and tax-clarity risk — the Schedule FA question is unsettled, and IFSCA/RBI rules around GIFT City fund structures are still relatively new and may evolve.

- Forex friction — banks charge a forex markup on outward remittances beyond TCS, and rebalancing back into rupee assets later means another round of conversion costs.

Should you invest?

You want genuine, uncapped US equity exposure.

You’re comfortable with LRS remittance and TCS.

You’re willing to file Schedule FA out of caution.

You can meet the $5,000 minimum comfortably.

The $5,000 minimum is a stretch right now.

You want to avoid foreign-asset tax reporting.

You need a simple SIP in INR without LRS complexity.

You’re only making a small, token allocation.

Frequently asked questions

Can NRIs invest in these PPFAS GIFT City funds?

No. The S&P 500 and Nasdaq 100 FoFs are structured for resident Indian investors under LRS. NRIs should look at PPFAS’s planned inbound fund — designed to channel NRI money into the Parag Parikh Flexi Cap Fund — or other NRI-eligible routes.

Is my existing PPFAS mutual fund KYC valid for GIFT City?

No. GIFT City investments need a fresh, separate KYC and folio. The GIFT City entity is a different legal entity regulated by IFSCA, not SEBI — even existing PPFAS investors must go through the process again from Step 1.

Is there a lock-in period or exit load?

No lock-in and no exit load. Units can be bought or redeemed on any business day. NAV is published daily in USD, and redemption proceeds are received in USD which you then convert to INR through your bank.

Do I pay capital gains tax separately when I redeem?

No. Tax is deducted inside the fund before the NAV is published. The NAV you receive on redemption is already net of tax — unlike a domestic mutual fund where you compute and pay capital gains yourself.

Do I need to file Schedule FA for these holdings?

This is currently debated among tax professionals and there is no definitive guidance yet. Most advisors recommend filing Schedule FA as a precaution, given the ₹10 lakh penalty under the Black Money Act for non-disclosure. Speak to a CA before you file. See our Schedule FA guide for details.

What happens to my LRS limit when I invest?

Every dollar you remit counts toward your USD 250,000 annual LRS limit, shared across all purposes — education, travel, investments. If you are also remitting money for other purposes, track your cumulative total for the financial year carefully.

Disclaimer: This article is for educational purposes only and does not constitute financial, legal, or tax advice. Tax laws and regulatory rules change frequently. Please consult a qualified chartered accountant or cross-border tax advisor before making investment decisions. Global Investing Sahi Hai is not a SEBI-registered investment advisor.